PVE’s Pensions Caused the Structural Deficits and Fiscal Instability

EXECUTIVE SUMMARY:

PVE’s rising Pension Costs and Debt are the cause of the City’s structural deficit. Residents placed Fiscal Stability as a priority over policing in the city’s survey (page 3). The Measure PF tax does NOT include pension funding, but does include increasing staffing from 57.5 (LINK) to 65 (page 8) , the highest level in the city’s history. THIS WILL ESCALATE DEBT GROWTH FASTER, because it does not include fully funding pensions, so more employees will have benefits funded by rising debt growth.

To eliminate our Structural Deficits we must pay the full cost of Pensions, rather than continuing to fund our city on unlimited rising debt. This year the city is paying $2 M in debt service for $20 M in debt. That is 10% in debt service alone, which does not include the semi-monthly payroll payments to CalPERs.

ADDITIONAL INFORMATION:

Pensions are THE CAUSE of the city’s Structural Deficits and Fiscal Instability LINK

How Pensions are Misunderstood, Underpaid and Explode in Costs LINK

Pension solutions: Stop new debt and Pay off existing debt LINK

PVE pays the Second Highest Pension Debt Service per Capita and Household in CA LINK

City Decisions that have Worsened the Situation and Lost Opportunities - Lessons need to be Learned LINK

Additional Issues and Impacts LINK

CA legislators are progressing a new law to spike pension benefits and pension costs while most cities are school districts are in the red with negative balance sheets already LINK (PVPUSD has a $40 million deficit on their balance sheet)

Bottom Line: LINK

Council unanimously endorsed the Measure PF tax that excludes pension funding and have not paid the full cost causing $20M in debt

For eight years, Council has not have the will to solve the problem.

It will require more funding or reduced expenses or a combination of both forever until addressed.

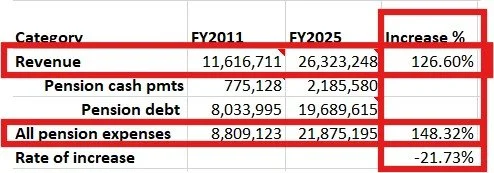

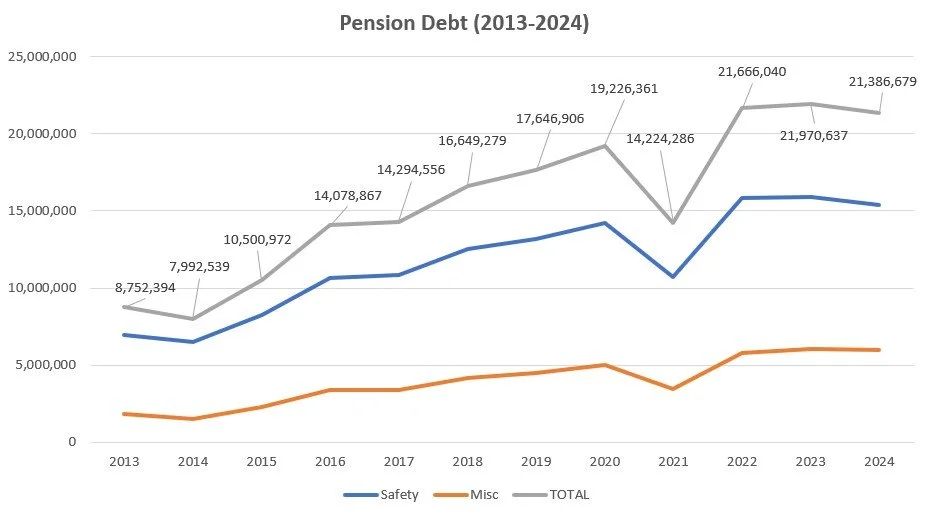

Structural Deficit over the last 15 years (2011-2025):

Pension expenses outpaced Revenue growth by 22%

Rather than pay the full pension expenses, the City created $13 M in new debt at 7% interest

Pensions are THE CAUSE of the city’s Structural Deficits and Fiscal Instability

IMPACT:

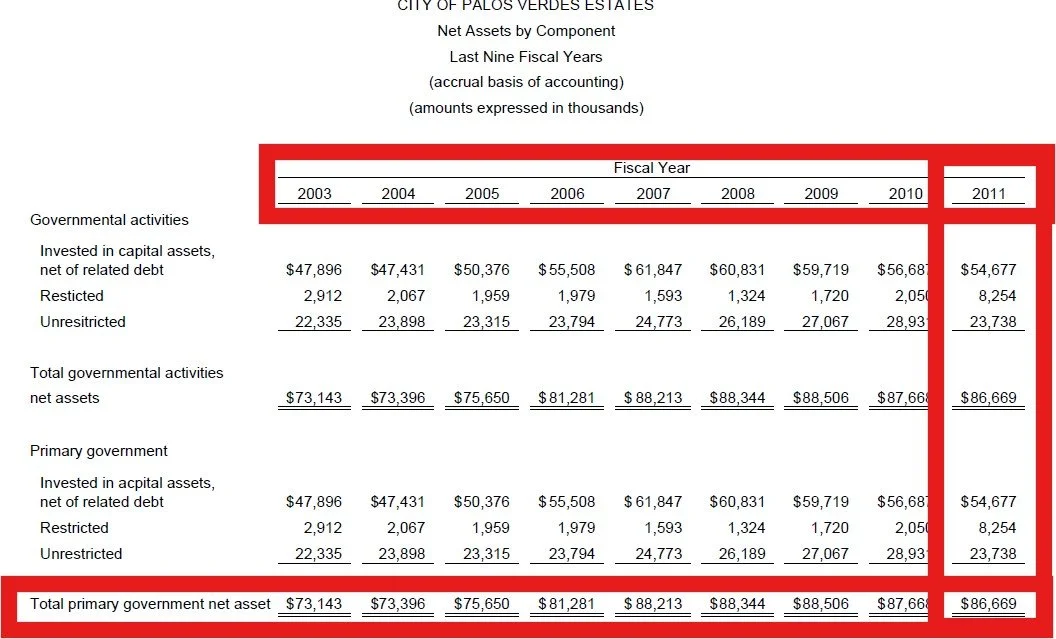

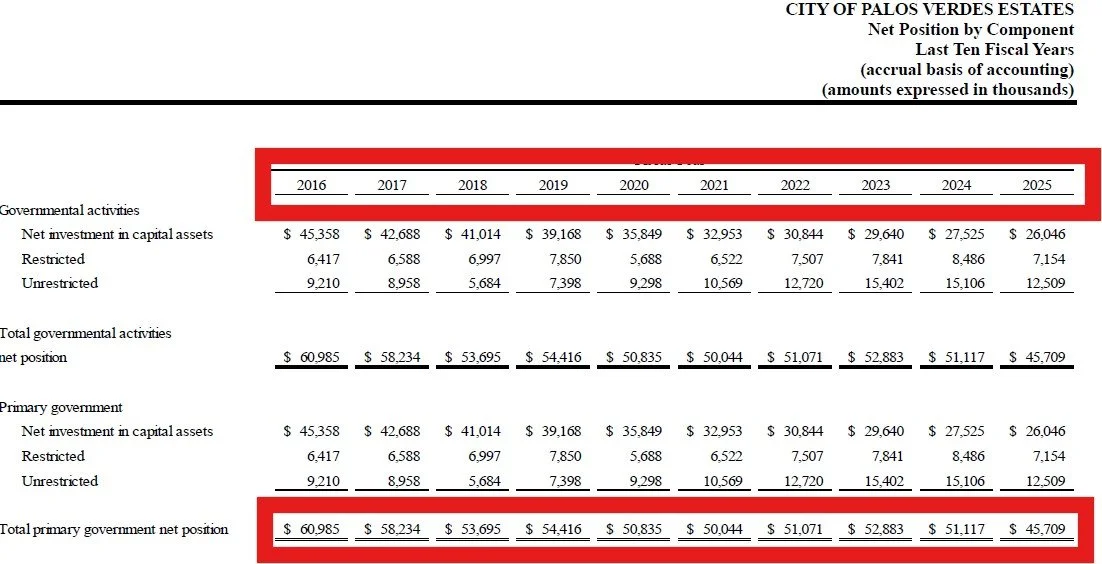

The City’s Balance sheet shrank by $33 M from 2011 to 2025

From $76.6 M to $45.7 M

The cost of pensions expenses during this period was $33 M

$20.3 M: payments made to CalPERs

$13 M: in incremental debt caused when the city short-payed the full expense (which CalPERS allows)

City docs sourced: Audited Reports: 2011 and 2025, CalPERs report, Finance Dept Pension costs report, FY2025 Budget. Note: GASB statement 68 required cities include pension debt in their financial reports starting in 2015, so 2011 was overstated by $8 M.

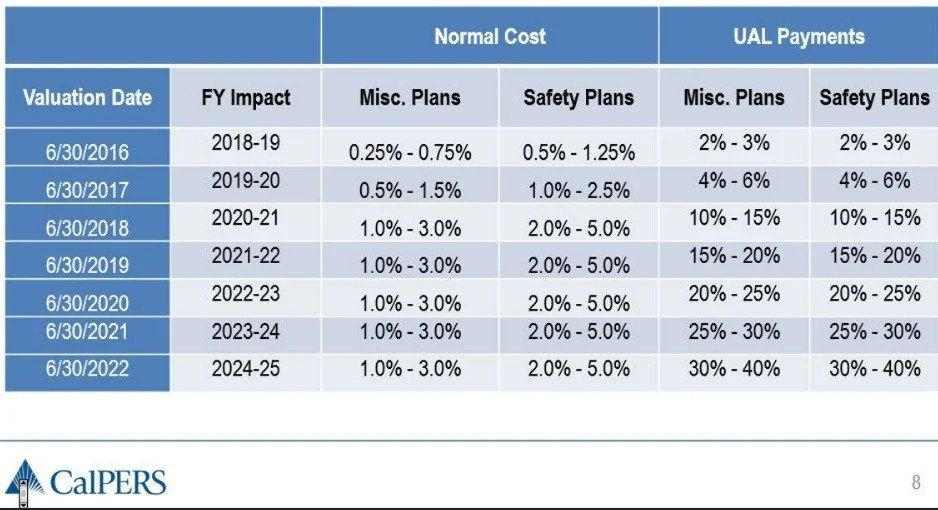

COSTS ARE ACCELERATING:

In 2016, CalPERs warned the rate of debt costs would accelerate faster over time, with significant increases compounded annually.

It has been 10 years and the City STILL has no plan.

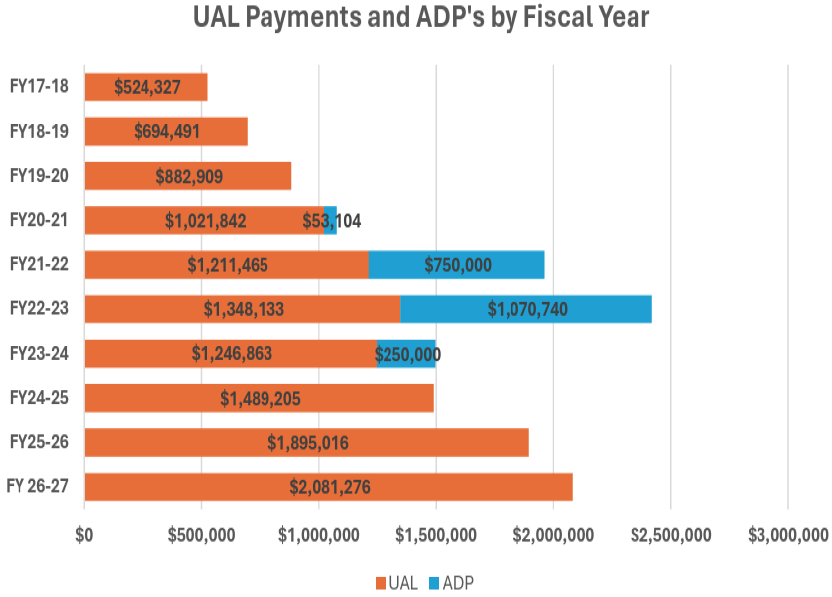

UAL payments (debt service) and ADPs (optional addition payments on the debt)

As warned, CalPERs’ requirement payments (UAL) continue to rise sharply. Every single year we are told things will magically turnaround in the future, but none of these “predictions” are based on core underlying facts that cause the costs to rise.

The City’s additional payments of $2 M were too low to have an impact.

A plan for Fiscal Stability begins with a FACT-Based costs and causes, and must include steps to mitigate the debt and cost increases using new revenue. The only way to prevent continued escalation of taxes for revenue is to address the cost drivers.

How Pensions are Misunderstood, Underpaid and Explode in Costs

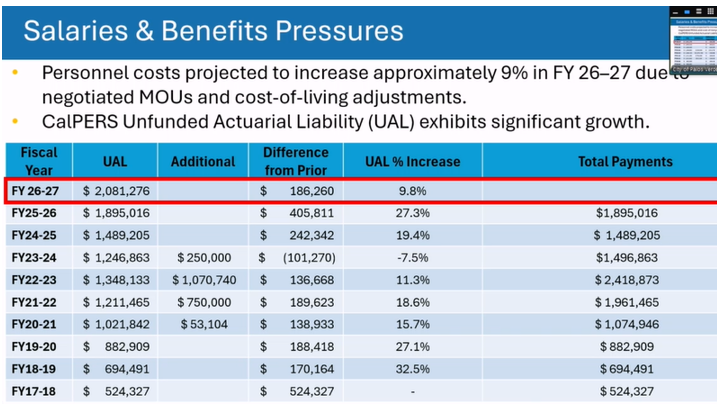

Shown is information provided to Council at a 3/10/2026 budget meeting.

This shows the extraordinary growth of pension debt payments, which is ascending quickly.

It illustrates Pension Debt (UAL) payments have tripled in the last 8 years.

But, this presentation did not include the full costs of pensions.

Full pension annual expenses are comprised of four pension expenses:

Not shown below: (which is additional millions)

The "Normal Payments" which is the employer contribution each pay period that should cover the full cost for that period (it doesn't, so it causes more debt)

The incremental debt increase because we short-pay each year causing debt to increase

Shown:

The annual Debt/UAL payments (sometimes it covers the 7% interest, sometimes it is a negative amortized payment that toss the interest payment into new debt and, infrequently, it includes a contribution to pay down the principal)

ADPs: These are discretionary volunteer payments to reduced debt (shown - called "Additional")

Staff received 9% compensation increases last year. It states due to cost of living and union contract (MOUs) negotiations. This a bit confusing because the COLAs are part of the increases in the MOUs. "MOUs" are union contracts with the city.

We don't pay the full cost of pensions, so pension debt explodes because it is tied to:

Pay increases (salary + other paid benefits)

Additional staffing

CalPERs under-performance of PVE's investments ($50 million) causing inadequate returns

Changes in the Union contracts where Council provides additional or increased benefits that are pensionable

CalPERs understates the necessary employee and employee contributions for each pay period, so the full cost is tossed into debt

Our Pension debt payments increased to $2.1 M - the grid in the next section below shows how fast these payments are accelerating.

Here is where it is misleading: the full annual expense of pensions are 4 things together, but they exclude 2 of them to understate the expense:

Not shown below:

The "Normal Payments" which is the employer contribution each pay period that should cover the full cost for that period (it doesn't, so causes more debt)

The incremental debt increase because we short pay each year causing debt to increase (not shown)

Shown:

The annual Debt/UAL payments (sometimes it covers the full 7% interest, sometimes it does not and sometimes it includes a contribution to paydown the principal)

The Discretionary volunteer payments to reduced debt (shown - called "Additional")

Look at the UAL/Debt increases year by year below - this is why we have a structural deficit.

Pension solutions: Stop new debt and Pay off existing debt

Both Pensions problems must be solved:

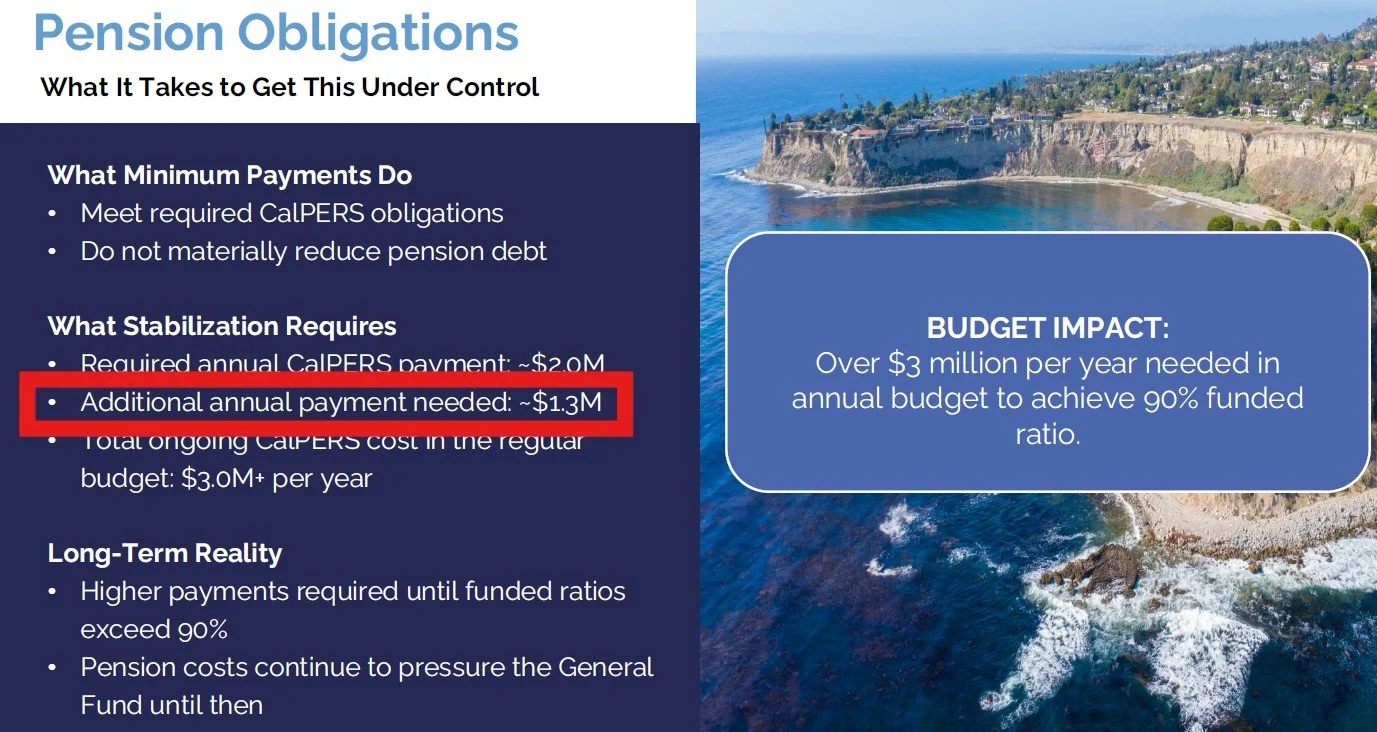

Stop debt growth ($1.15 M annually)

Pay down existing debt ($20 M)

1. Stop debt growth: city must pay $1.15 million more a year

This graph shows the city pension debt increased an average of $1.15 million a year when the city only paid the required CalPERs payments.

To simply stop the bleeding, the City must pay $1.15 million more every year — just to prevent the debt from rising further

After Council implements their plan to increase staffing to a 25 year high (page 3), and provide salaries that increase faster than inflation, this will accelerate..

2. Pay down existing debt and save the 7% high interest

The City owes $20 million in pension debt at 7% interest, costing taxpayers $1.4 million annually in interest alone.

The Council claims (Page 14) that paying an additional $1.3 million per year will reduce debt by 90%. But:

The June tax measure does not fund pensions. HOWEVER, it does include increasing the staffing levels to the highest in city history, so it will increase the pension crisis.

This forces Residents to pay for ANOTHER tax

Of the $1.3 million CalPERs payment the City proposes, $1.15 million would merely stop new debt growth

This leaves only $150,000 per year to reduce the debt

At that pace, it would take over a century to reach 90% funding — assuming no new benefit increases, no additional staffing, and no higher salary growth.

Shown above: Page 14 of the City’s State of the City Presentation

PVE is an Outlier

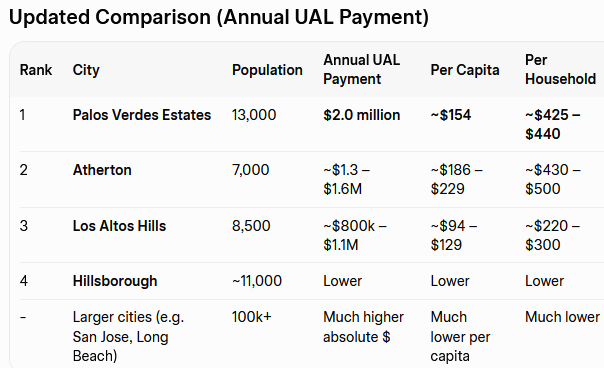

PVE pays the Second Highest Pension Debt Service per Capita and Household in CA

Second only to Atherton, PVE pays more for pension costs than any other CA city.

SOLUTION:

If PVE used a temporary tax to pay down the pension debt, this would redirect $2 M to infrastructure.

PVE pays 3.5-6 times more than the average CA city per capita for pension debt service annually.

Council Actions

Decisions that have Worsened the Situation and Lost Opportunities - Lessons need to be Learned

10/08/2020: the Council’s Pension Adhoc presented their working group’s recommendation to pay down the pension debt using a temporary tax Report. Council did not deliberate or approve the recommendation VIDEO - which would have saved millions by now. The city now pays $2M annually in debt service, increasing annually, which should instead have been directed to Infrastructure.

5/10/2022: Council passed a “pension policy” POLICY to pay down the debt, without a means to fund it. Predictably, it failed within a year.

3/24/2026: Council held a meeting VIDEO and “concluded” they could pay off $20 million in debt with only $7.8M - by stating CalPERs, despite it’s history, would somehow better investment results to fund PVE pensions.

However, the Pension presentation understated the future pension costs by using FALSE information as input into GovInvest, PVE pension projection tool:

It only included 1 or the 2 pension plans

It excluded the new hires expected for all the open positions

It showed 3.5% expected annual increases, but the budget shows they plan 4.5%

It did not include all the other pensionable pay categories (like 10% salaries increases for a degree, pensionable overtime, etc.)

It excluded the 20% COLA just provided to employees (2024: 10%, 2025: 6%, 2026: 4%)

It excluded the annual 5% merit increases

The erroneous conclusion presented: they can pay off $20 million in debt with $7.8 million and they can ignore the fact that they continue to underpay the cost thereafter which causes more debt again.

Additional Issues and Concerns

Council erroneously believes if CalPERs makes a return of 6.8% we break even for the year. Not True:

The 6.8% assumed rate of return is net of administrative expenses. This means the investments must earn roughly 7.0%+ gross just to net 6.8% after fees and costs.

CalPERs only provides investment returns for the “funded” portion of our liabilities. PVE is only ~85% funded. So, the city pays the 7% investment returns for the unfunded portion (~1.4 M) which is included in the debt service which has climbed to $2 M annually)

The payroll payments to CalPERS (aka “normal costs”) are underfunded, so the rest becomes debt.

Other issues that hide costs:

In years when CalPERs’ performance is particularly bad, they lower the compulsory payments below the 7% interest, to “smooth” the costs, so the unpaid interest is just added to the debt (a negative amortized payment).

The City Balance sheet has fake assets called pension inflow/outflow items. These are used to “smooth” (hide) CalPERs passed investment losses of our money we has already paid for future pension payments. Over time, these fake assets are removed which results in a lower, but more accurate, Balance sheet. Municipal balance sheets are called the “Net Position” statement.

CalPERs is run by Wilshire

Why It’s Difficult to Consistently Hit 7% investment returns

High valuations in stocks and private equity make future returns harder.

Private equity valuations are not “standardized” and are often overvalued

Lower bond yields than in past decades limit fixed-income returns.

Heavy reliance on private equity and alternative investments — which are volatile and have high fees.

Most independent forecasts for diversified portfolios like CalPERS’ project forward returns in the 5.5% – 6.5% range over the next 10 years.

Bottom line: CalPERS has a good chance of beating 6.8% in strong market years, but consistently achieving 7%+ over the long term looks challenging.

Conflict of Interest

Wilshire Associates is by far the most influential consulting firm at CalPERS in deciding the asset allocations, investment policy and risk management decision

BUT IT GETS FAR WORSE

The State is progressing efforts to increase Safety (Police) retirement benefits

State lawmakers have re-submitted bill AB 1383, which would boost pensions for safety employees without setting aside funds to meet these pension payments. This means debt will jump overnight. This is the same lethal combination that led to a 10x increase in annual pension spending and debt since 2000.

THE BOTTOM LINE

Effective Leadership Requires Problems are Faced with Facts

Without Structural reform (more money, reduced costs or both), taxpayers face rising costs with no path to fiscal stability.

The City’s plan is to kick the can down the road by passing a massive June tax, that excludes pension reform and pension funding. Then, using these funds, Council plans to increase staffing by 13% to the city’s highest historical level of 64.5 (page 3) without fully funding the full costs of pensions. This will exacerbate the problem and cause more debt.

April 13, 2021: The Council tossed a year long study with real solutions without explanation VIDEO Presentation, that used financial projections based on facts and historical trends. Inaction has caused these funding solutions to increase.

May 10, 2022: The Council created a failed “Pension Policy” using unrealistic projections. Worse, it required funding the city had neither the will or the means to provide. This resulted in debt growth expansion with increased costs. Residents provided the facts VIDEO to Council informing them of their policy’s predictable failure, but Council remained non-responsive and passed the policy without addressing facts provided.

Further information to understand pensions: LINK.